.png)

Stablecoins for Payments: Who’s Actually Using Them?

- May 19, 2025

- 5 min read

Updated: Dec 18, 2025

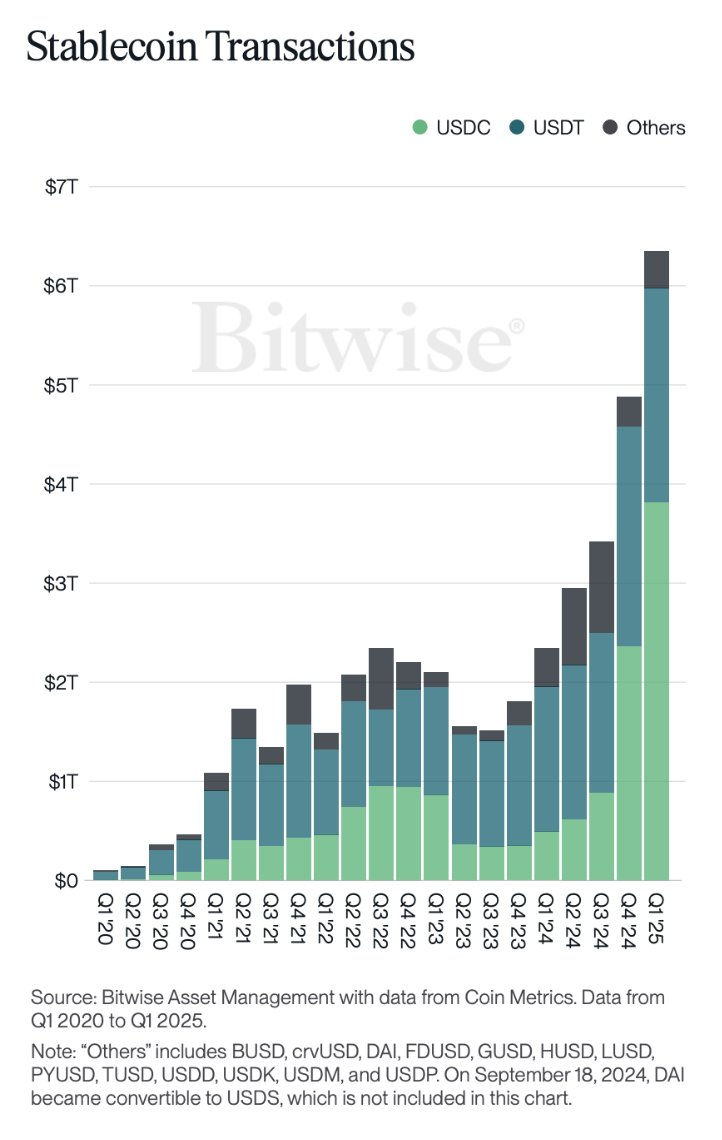

Stablecoins Beyond Speculation—Payments Already Running Worldwide

Stablecoins were once mostly used by crypto traders to move funds between exchanges without relying on banks.

That utility has grown.

Today, people use them to settle freelance invoices, reload ride credits, pay rent, and top up wallets.

Major companies have rolled out stablecoin support in a real way.

Stripe supports USDC payouts for global creators.

Coinbase lets users send stablecoins abroad with zero fees through its smart wallet.

Shopify gives merchants tools to accept stablecoin payments.

Visa processes onchain transactions directly.

Grab users in Southeast Asia buy credits using stablecoins for daily transport.

These are not experiments or future features. They’re active, working systems used across borders.

In parts of Latin America and Southeast Asia, this matters even more. With inflation hitting local currencies hard, stablecoins help people keep their money steady and accessible — no middleman, no delays.

What’s happening isn’t loud. No headlines. No token launches.

Just a gradual rollout of options that already fit into the routines of people who need faster, cheaper ways to pay.bills—leveraging stablecoins as a reliable alternative to local currencies facing volatility.

The Retail Pilot That’s Live

Shopify merchants have integrated USDC stablecoin payments through Stripe, facilitated by the Solana blockchain. Unlike announcements often exaggerated for effect, this integration quietly became operational. Merchants can now seamlessly accept stablecoin payments, effectively bypassing traditional bank payment delays.

Solana's blockchain serves a clear function in this context—it ensures transactions settle rapidly and cheaply, significantly reducing overhead costs typically associated with credit card processing or bank transfers. Stripe manages the frontend integration, ensuring merchants see nothing complex, only an easy, reliable method of receiving payments. Consumers experience an intuitive, uncomplicated checkout experience identical to traditional payment methods.

This practical, behind-the-scenes implementation signals a broader acceptance of stablecoins within retail commerce, not as speculative instruments, but as legitimate, efficient financial tools.

A New Payment Pathway

Visa has officially begun settling treasury transactions using USDC on the Ethereum and Solana blockchains. This implementation represents more than a symbolic gesture—it’s a fully operational integration. Visa's network now processes cross-border transactions seamlessly, bypassing traditional financial intermediaries.

Visa's adoption of USDC is particularly relevant for international payments, where conventional banking methods can involve delays, additional costs, and multiple intermediaries. By directly leveraging blockchain technology, Visa offers its corporate clients reduced friction and improved efficiency.

The real-world effectiveness of Visa's approach has encouraged other financial institutions to seriously consider stablecoin integration as a realistic solution to existing payment infrastructure limitations.

Practical Digital Payments in Southeast Asia

Grab, a major player in Southeast Asia’s digital economy, now allows users to convert stablecoins into GrabPay credits through StraitsX. This integration provides everyday practicality without drawing attention to its underlying technology. Users effortlessly fund GrabPay accounts using stablecoins, streamlining everyday expenses such as meals, transportation, and small retail purchases.

This approach showcases the viability of stablecoins beyond speculative trading, positioning them as practical digital currencies. In a region known for rapid digital adoption and mobile payments, Grab’s strategy aligns perfectly with consumer needs, minimizing dependence on traditional banking structures.

Grab’s collaboration with StraitsX represents a notable step towards mainstream acceptance of stablecoins, emphasizing convenience, reliability, and ease of use. Such integrations set a compelling example for future adoption in other regions and industries.

A Cautious Step Toward Digital Dollar Usage

PayPal introduced PYUSD, its own stablecoin, in a controlled and methodical rollout. While initial adoption rates have remained modest, the stablecoin has established itself within PayPal’s ecosystem as an active financial tool. Users currently buy, sell, and transfer PYUSD within the app, taking advantage of simplified digital dollar management.

Although the integration remains confined largely within PayPal’s internal network, it demonstrates a practical use case for stablecoins by an established financial platform. PayPal’s cautious yet deliberate entry underscores growing confidence in stablecoins as feasible payment alternatives. This careful progression provides valuable insights and sets the stage for potential broader acceptance within the global financial ecosystem.

Stablecoins in Argentina, Turkey, and Nigeria

In countries like Argentina, Turkey, and Nigeria, stablecoins have become essential tools for everyday financial transactions. These nations face frequent economic fluctuations, unstable currencies, and restrictive monetary policies. Stablecoins offer practical, immediate financial relief, enabling citizens to preserve purchasing power and securely manage their financial resources.

Platforms and apps in these regions now facilitate stablecoin transactions, making digital dollar access straightforward and reliable. Stablecoins serve more than just a financial function—they represent economic stability and predictability in unpredictable economic conditions. Their adoption in these countries underscores their potential as genuine alternatives to traditional currency systems, revealing a broader global shift towards practical digital financial solutions.

What’s Working, What’s Not

Several factors currently drive stablecoin adoption in real-world payments: ease of use, speed, and cost-effectiveness. Transactions processed via stablecoins generally settle faster and incur lower fees compared to traditional banking systems. This efficiency appeals strongly to merchants and consumers alike, particularly in international transactions.

However, challenges remain. Regulatory uncertainty presents substantial hurdles. Tax implications for stablecoin transactions are often unclear, creating hesitation among potential users. Inconsistent wallet support and inadequate fiat-to-stablecoin exchange mechanisms further complicate widespread acceptance.

Addressing these practical limitations will determine the future trajectory of stablecoins in everyday payments. Clearer regulatory frameworks, improved user experience, and robust support infrastructure could accelerate adoption and unlock stablecoins' full potential as viable payment alternatives.

Stablecoins as Dollar Access

Stablecoins have emerged as reliable alternatives to traditional currency methods, particularly in regions with limited access to stable currencies or banking infrastructure. They offer practical solutions for storing value, conducting cross-border transactions, and mitigating currency instability.

This practical usage of stablecoins represents a major development in financial inclusion, providing populations traditionally underserved by banks with robust financial services. By enabling individuals and businesses to hold stable currency equivalents easily accessible on mobile devices, stablecoins redefine how currency availability and economic empowerment can be approached globally.

The widespread adoption of stablecoins as viable currency alternatives marks a notable development in digital finance, influencing how financial stability and economic participation can evolve worldwide.

Stablecoins in Payments

Stablecoins have firmly established their place within the broader financial ecosystem, evolving beyond niche financial instruments. Their integration into everyday payments marks a genuine advancement in digital finance, highlighting their practical and immediate benefits.

The continued development of stablecoin-based payment methods depends on addressing regulatory clarity, improving user experience, and expanding infrastructure support. Each successful use case provides further evidence of their effectiveness, inspiring greater confidence and wider adoption across industries.

As stablecoins steadily become integrated into global payment systems, their potential to transform financial transactions continues to grow, offering compelling opportunities for businesses and individuals alike.

🎥 Watch the Video

For a quick video version of this post, watch my YouTube video: Stablecoins for Payments — Who’s Actually Using Them?

🗣️ Join the Conversation

Blockchain and Web3 Insights LLC is committed to delivering fact-based, practical education on Bitcoin, blockchain, and decentralized technologies. If this article was useful, please share it with your network and connect with us through the channels below to continue the conversation.

🔗 Stay Connected:

YouTube: Blockchain and Web3 Insights

Twitter/X: @Ajay8307

Bluesky Social: @blockchainweb3

Instagram: blockchainandweb3

Threads: @atom8307

Medium: Blockchain and Web3 Insights

LinkedIn: Ajay Tomar

📩 Subscribe to My Newsletter:

Stay current with Blockchain & Web3 Weekly Bytes, published every Saturday. Each edition includes:

Clear insights on Bitcoin, blockchain, and digital assets

A weekly trivia feature

Practical updates designed for learners, teams, and professionals

📚 Educational Resources:

⛔️ Disclaimer ⛔️

This article is for educational purposes only and is not financial advice. Do your own research and consult a professional before making any investment decisions. Some links may be affiliate links that support Blockchain and Web3 Insights LLC at no extra cost to you.

Comments